I recently came across this great free cloud accounting for UK users http://www.quickfile.co.uk

Accounting for a loan so that Balance Sheet and Profit & Loss are correct was a little confusing so I put this article together.

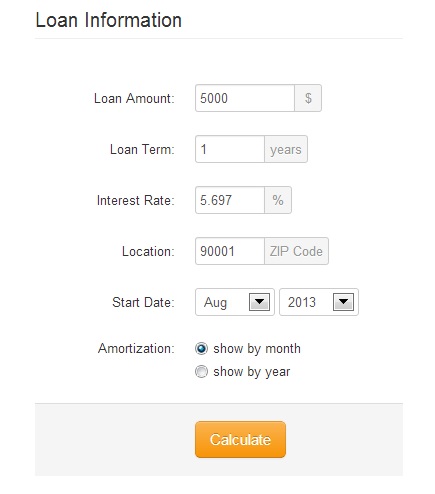

Example £5000 loan over 12 months, annual interest rate 5.697%, taken out 1-Jul-2013, first payment due 1-Aug-2013

(EDIT – Dec-2015, I’M NO LONGER RECOMMENDING QUICKFILE)

STEP 1 – Amortisation (Amortization if your American)

Assuming that loan interest is calculated monthly, we need to work out how much is interest and how much is capital repaid. A tool that useful for this is Amortization Schedule Calculator, for example :

This will produce (don’t worry about dollar amounts, the calculations are the same for UK pounds or any currency) :

Amortisation Schedule

| Date | Interest | Principal | Balance |

|---|---|---|---|

| Aug, 2013 | $23.74 | $405.90 | $4,594.10 |

| Sep, 2013 | $21.81 | $407.83 | $4,186.28 |

| Oct, 2013 | $19.87 | $409.76 | $3,776.51 |

| Nov, 2013 | $17.93 | $411.71 | $3,364.81 |

| Dec, 2013 | $15.97 | $413.66 | $2,951.15 |

| Jan, 2014 | $14.01 | $415.63 | $2,535.52 |

| Feb, 2014 | $12.04 | $417.60 | $2,117.92 |

| Mar, 2014 | $10.05 | $419.58 | $1,698.34 |

| Apr, 2014 | $8.06 | $421.57 | $1,276.77 |

| May, 2014 | $6.06 | $423.57 | $853.19 |

| Jun, 2014 | $4.05 | $425.59 | $427.61 |

| Jul, 2014 | $2.03 | $427.61 | $0.00 |

So repayments are £429.64 per month, capital and interest payments vary over course of loan. You could also use Excel or get the schedule from your loan provider if this is easier.

STEP 2 – Setup the loan account in Quick File for balance sheet

Go to your bank accounts, and press the “+” button to add a new loan account :

![]()

Enter details for your loan account (which will appear on balance sheet under liabilities):

STEP 3 – Money arrives in your bank account

Once the loan has arrived and showing in your current account, you need to tag it so it will show in your loan account in quick file :

You will now have your loan (principle amount £5000) showing in your loan account and also on your balance sheet under liabilities.

STEP 3 – Accounting for your interest

Several ways to do this. For this example I will use journal entries for each of the interest amounts, twelve amounts :

So there is a credit to your loan account, and a debit to account 7903 Loan Interest Paid. Do a journal entry for each interest amount, so :

1-Aug-2013 – £23.74

1-Sep-2013 – £21.81

1-Oct-2013 – £19.87

and so on …

Alternatively you could do one journal entry for each year (for a longer term loan). My loan I just put one amount for the total of interest amounts within the tax year and posted it on the last day of my accounting year.

STEP 4 – What to do with your monthly payments

When mortgage payments show on your bank statement you need to tag them against the loan account, exactly as you did in STEP 3.

That’s it…… interest amounts will now show in your profit and loss, balance sheet will reflect the current balance of your loan account. Properly accounted for!

I use quick file for my accounts based in UK, it’s the best thing I’ve found for this, absolutely awesome check it out – http://www.quickfile.co.uk

Useful pages, used for research :

http://www.principlesofaccounting.com/chapter13/chapter13.html

http://community.quickfile.co.uk/quickfile/topics/mortgage_repayment

http://www.amortization-calc.com/

http://www.uktaxandaccounts.com/index.php/Preparation-of-Accounts/long-term-loans-and-interest.html